Can investors really be that wrong? Global risk is today greater than ever in history and at the same time the great majority of investors show no fear at all. There are so many potential catalysts that could shake the world economy out of its sweet dreams into a living nightmare that it is impossible to forecast where the trigger will come from. It could be a debt collapse in Japan, China, USA, Eurozone or emerging markets. Or it could be a currency collapse in any of those regions. Or it could be a stock market collapse, or it could be……, or it could be……

Many stock markets around the world are at all-time highs. But there is no fear and no serious selling. Any slight decline is a buying opportunity. The S&P is up 4x since 2009 but that does not make investors nervous. That markets have been fuelled by dangerous and unsustainable credit expansion does not concern markets. Not even that global debt has doubled since 2006.

CHANGE STARTS IN THE PERIPHERY

But change starts in the periphery where very few are looking. Look at China where the Shanghai composite is down 23% since January. And look at Brazil where the Bovespa is off 17% so far this year and Turkey which has lost 20%.

What is important to understand is that most major markets are now looking extremely vulnerable, be it Japan, Germany or the US. Fundamentally most markets are overvalued with the help of central bank liquidity. Also, technically we are not far from crashes in most markets. Whilst there is always a possibility of a last hurrah, it looks like all markets have topped, including the US, and that later in 2018 we will see major falls. Once the bear markets start, they are likely to turn into secular trends that last many years and result in falls of 75% to 95%. Difficult to believe for most investors today, but nobody in 1929 believed that the Dow would fall 90% in the ensuing years and take 25 years to recover.

PROSPERITY BUILT ON DEBT IS SHORT LIVED

The investment world has been lulled into a permanent state of security and euphoria. Hard to deny that central banks and governments have been extremely skilful in telling the world constant lies. And why would anyone protest, as the rich are getting incredibly rich and many normal people in the West have a higher standard of living than ever. Very few of the “normal people” understand that their prosperity is built on personal debt and their government borrowing more than ever. Nor do they understand that they are responsible for this debt that they of course can never repay.

Even less do they understand that they will be on their own when debt implodes and they lose their jobs. Because the state will at that point have run out of money and there will be no social security or unemployment benefits. Nor will there be any pension for retirees as pension funds will go from extremely underfunded to totally unfunded.

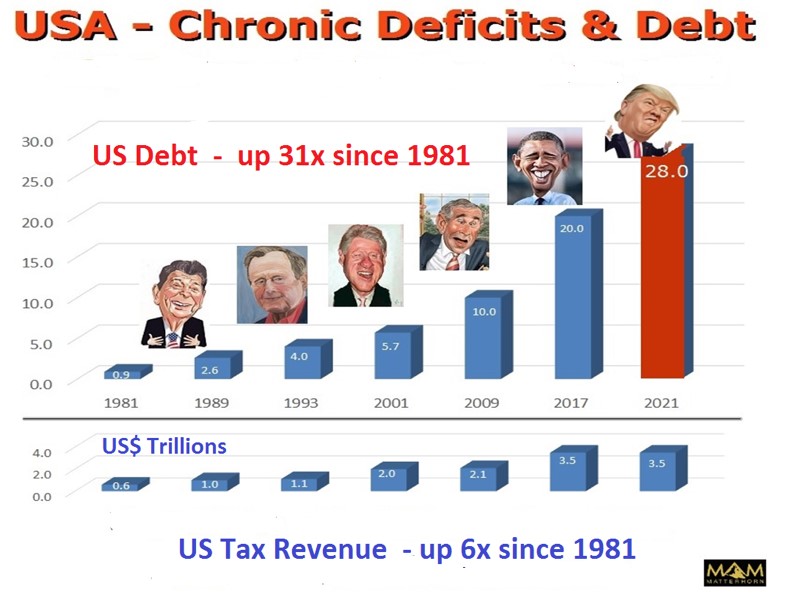

US DEBT DOUBLES EVERY 8 YEARS – $40 TRILLION IN 2025

When Trump was elected in November 2016, I forecast that US debt would continue to double every 8 years on average, as it has done since Reagan become president. That would lead to $28 trillion debt by 2021 and $40 trillion by 2025.

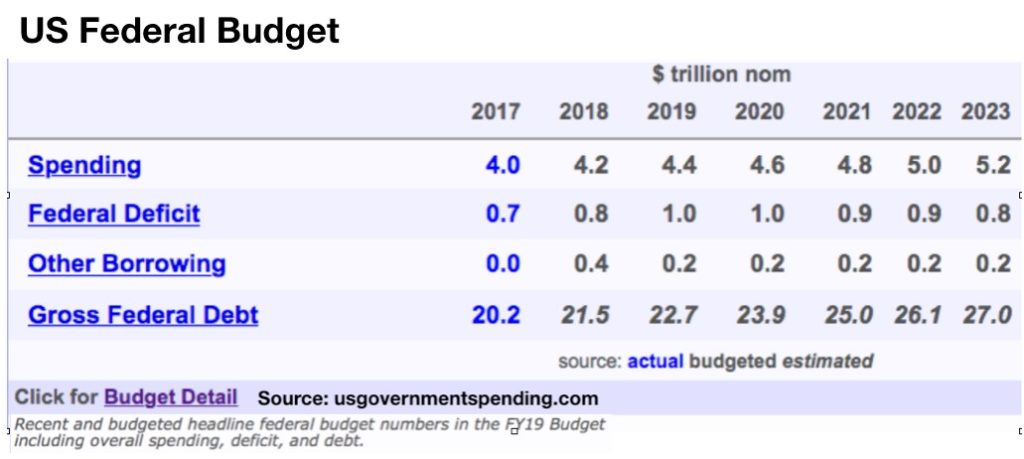

Well, it seemed quite unrealistic back in 2016 that the US would average over $2.5 trillion deficit in the ensuing 8 years to 2025. Judging by current forecasts, it looks like debt will “only” be $25 trillion in 2021.

But as tax revenues decline and spending increases, I would not be surprised to see $28 trillion debt in 2021. That would put the US on course for a $40 trillion debt in 2025. That would mean a doubling of the debt from 2017 which is in line with the historical trend of a 100% increase every 8 years.

INTEREST COSTS WILL EXCEED TAX REVENUE

A $40 trillion debt in 2025 would be bad enough but things are likely to get worse. With debt exploding, the Fed will lose control of interest rates as foreign investors dump US bonds. A rate of 10% at that point would not be unrealistic. That would lead to an interest bill of $4 trillion per year (10% on $40T). This would mean that just interest costs are likely to be higher than total tax revenue.

So the US is on the cusp of a deficit and debt explosion of catastrophic proportions. And this forecast does not include major problems in the financial system, leading to additional money printing as well as a collapsing dollar.

US MUCH WORSE THAN EUROPE

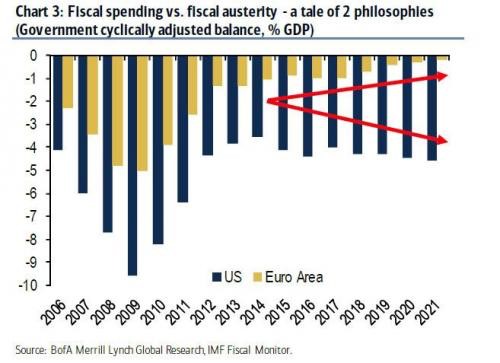

With the US by far the biggest threat to the global economy, the world focuses on the problems in the EU. Yes, there are major problems in Greece, Italy, Spain and many more European countries as well as in the European banking system. But relatively, the fiscal controls in the EU are far more disciplined than in the US. Just look in the chart below at the Eurozone austerity compared to the US profligacy.

Whilst the US deficit is forecast to continue at around 5% of GDP, the Eurozone is running at 1% or less. There is a consensus that many of the Eurozone countries are basket cases and that is hard to argue against. Very few talk about the US as a basket case. But with no real budget surplus since 1960, the US financial and military hegemony will soon come to an abrupt end, especially since deficits are likely to increase further in the next few years.

So as the currencies continue their race to the bottom, (see last week’s article), the US dollar is likely to beat the Euro to Zero. But it really doesn’t matter who will be first to the bottom in a race that only has losers taking part.

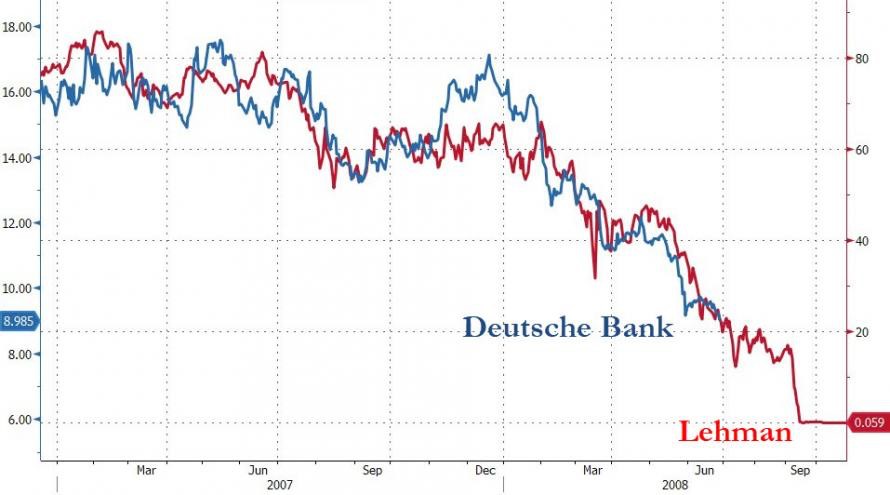

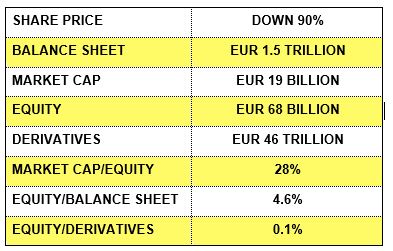

DEUTSCHE BANK – THE NEXT LEHMAN

Another potential catalyst could be one of the world’s biggest banks which has a balance sheet and share price which look extremely ominous. Deutsche Bank (DB) has fallen 90% from 2007. The chart looks very similar to Lehman in 2008 just before it collapsed.

The market clearly sees the writing on the wall. The share price only needs to drop another 10% from the top to go to Zero. That is why no one believes that DB is even worth the equity as the market cap is only 28% of shareholders’ funds. A 4.6% loss on the DB loan book or a 0.1% loss on the derivative portfolio would totally extinguish the equity. Both these events are very likely to take place within the next few years.

Every single statistic of DEUTSCHE BANK looks frightening:

Since DB is virtually part of the establishment, the German government would do everything within its powers to save the bank. But how can they save a bank with a balance sheet of 50% of German GDP and a derivative portfolio of 14x GDP? Well they can’t but they will probably try. And the consequences are very clear: Welcome to Weimar II with unlimited money printing.

But no one must think that DB is the only bank in trouble. JP Morgan for example has $50 trillion in derivatives, 2.5x US GDP. And the Swiss banking system is 5x Swiss GDP, just to mention a few.

The fractional banking system is soon coming to an end with the most massive bang. Holding physical gold seems like an excellent idea!

Original source: Matterhorn - GoldSwitzerland

Reproduction, in whole or in part, is authorized as long as it includes all the text hyperlinks and a link back to the original source.

The information contained in this article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell.